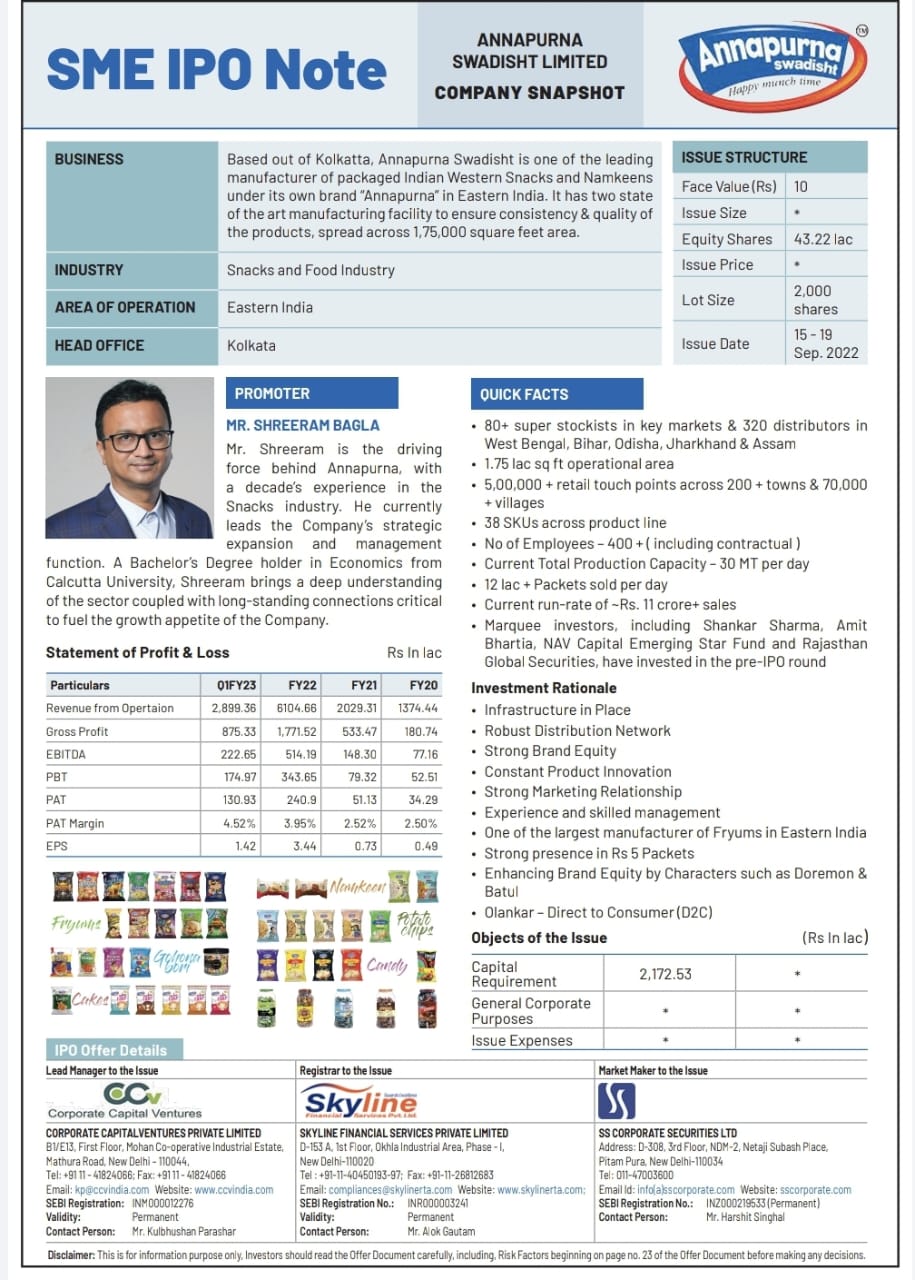

Do you know that the acquisition of any business now entails extra financial reporting requirement from Acquirer in the form of Purchase Price Allocation (PPA). Every company which has acquired any business recently, then on completion of acquisition, all of the assets must be valued. The basic concept of Purchase Price Allocation for Financial Reporting is that the purchase consideration paid under the transaction shall be allocated to:

- The assets acquired under transaction.

- Any excess consideration paid shall be allocated to goodwill or any deficiency shall be reported as gain from bargain purchase (arise in rare case).

Purchase Price Allocation Framework

Ind-As 113 Fair Value Measurement and Ind-As 103: Business Combinations provide framework for Purchase Price Allocation. A summarised framework of Purchase Price Allocation is given hereunder:

Why You Need An Advisor

Identification of Acquirer : Ind As 110 defines acquirer as the entity that obtains control of another entity.

Determination of Acquisition Date : The date on which the acquirer obtains control of the acquiree is generally the date on which the acquirer legally transfers the consideration, acquires the assets and assumes the liabilities of the acquiree—the closing date. However, the acquirer might obtain control on a date that is either earlier or later than the closing date. All pertinent facts and circumstances should be considered in identifying the acquisition date.

Determination of Purchase Consideration : The Purchase consideration can be defined as aggregate of the following:

Cash

Shares or Stocks at Fair Value

Deferred Consideration at Present Value

Contingent Payments at Fair Value

Liabilities

Identification and Valuation of assets acquired : All the Assets of Acquiree under each category i.e. Tangible, Intangibles are identified and valued.

Allocation of the Purchase Consideration : The Purchase consideration determined is allocated to the identified Tangible, Intangible and Monetary assets. Any amount of consideration paid in excess of assets acquired under transaction is recognised as Goodwill. In rare cases it may happen that assets acquired under transaction exceeds purchase consideration, which result in gain from bargain on purchase price

Importance of Purchase Price Allocation

Ind AS 102 does not direct the adoption of any specific method for valuation. If we refer the definition of fair value which is prescribed under Ind AS 102, fair value means:

PPA is a complex task and have impact the Financial Statements of the Company which ultimately have impact on the returns of the shareholders. A minor negligence in PPA exercise can land a Company into great trouble. The few negative impacts on business of the Company due to improper PPA are as under:

- Overstatement or understatement of Depreciation which in turn may understate or overstate the profits.

- Overstatement or understatement of Depreciation which in turn may understate or overstate the profits.

- There may be risk of Goodwill impairment

Our Role

CCV has a team of experienced Professional from various discipline having considerable experience in implementing Purchase Price allocation in most effective and efficient manner.